.jpeg)

What the State Farm settlement means for survivors in Malibu, Pacific Palisades and Altadena, and how rebuilding with fire-resistant means and methods can protect the insurability of your home or business for good.

If you lost your home in the Palisades or Altadena fires, the past year and a half has been one of the hardest of your life. The shock. The grief. The temporary housing. The insurance calls that circle back to nowhere. You're making impossible decisions while managing difficult emotions.

We don't lead with this to set a tone. We lead with it because it's true, and because everything else we say should be heard in that context.

Now there's a new development. State Farm, California's largest home insurer, has finalized a settlement locking in a 17% rate increase for homeowners, including tens of thousands of policyholders in the hardest-hit fire zones. We want to explain what it actually means, and then we want to share something that, genuinely, could change the timeline on your rebuild.

What Did the State Farm Settlement Decide for LA Homeowners?

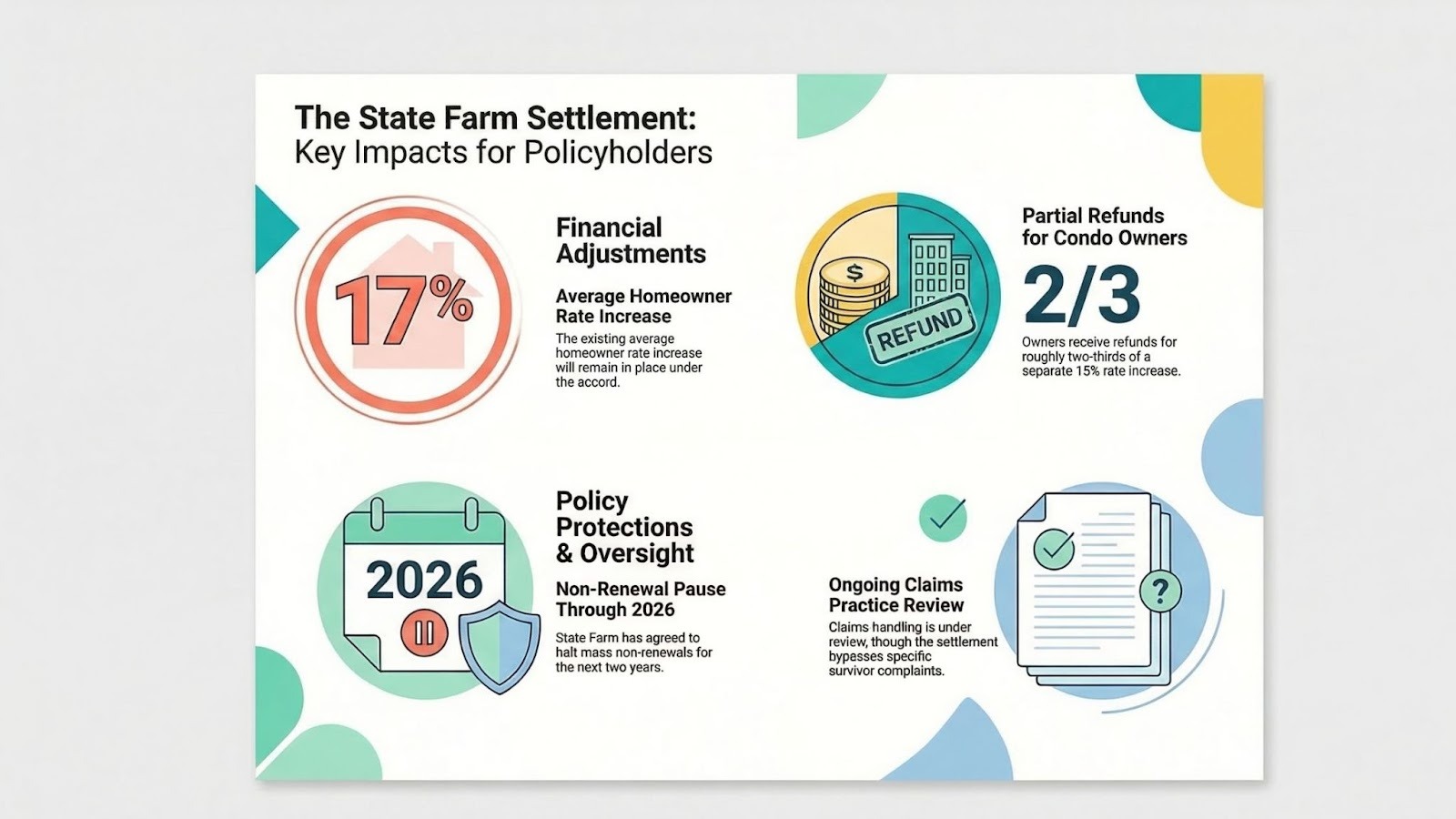

On March 7, 2026, a settlement was filed with a California administrative law judge that cements State Farm's emergency rate hike. A $530 million adjustment negotiated with Insurance Commissioner Ricardo Lara in the aftermath of the January 2025 wildfires.

The numbers behind it are staggering. State Farm reported paying $6.2 billion in wildfire-related claims last year, with an additional $1 billion still expected. The Palisades and Eaton fires together destroyed at least 16,000 homes and triggered more than 42,000 insurance claims. Across all insurers, more than $22 billion in claims has been paid to date.

Under the settlement:

- The 17% average homeowner rate increase stays in place.

- Condo owners will receive partial refunds (roughly two-thirds of a separate 15% increase).

- State Farm agrees to pause mass non-renewals through 2026.

- A review of State Farm's claims-handling practices is ongoing, but the settlement doesn't directly address survivor complaints.

One Malibu homeowner's premium reportedly jumped from $3,500 to $8,400 in a single year, while he remained in a 14-month dispute over fire and smoke damage. That story is not unusual. Many Pacific Palisades and Altadena survivors have reported low payout offers, denied toxin testing requests and delayed living expense reimbursements.

The settlement doesn't fix any of that. And for those still fighting their claims, it's reasonable to feel let down.

What the settlement does confirm is this: the California home insurance market is under structural pressure that isn't going away. As of early 2026, only 28 homes have been fully rebuilt out of more than 13,000 destroyed. Permitting is moving faster than expected in fire zones, averaging roughly 100 days, but insurance uncertainty is stalling rebuilds before they even start. The question of insurability is now central to every decision about how, whether and where to rebuild.

Can How You Build Your Home Actually Affect Your Insurance Rates?

Here's something that gets lost in the insurance news cycle:

Insurers don't just look at where your home is. They look at what it's made of.

Homes built with non-combustible materials carry a fundamentally different risk profile. That distinction, materials and construction methods, are increasingly shaping what coverage looks like, whether it's available at all, and how much it costs. For homeowners rebuilding in high-risk fire zones in Los Angeles, this is not a footnote. It may be the most consequential decision in the entire rebuild.

At Letter Four, we work with advanced non-combustible construction technology: fiber-reinforced concrete panel systems with no wood framing, no combustible soffits or trusses. The walls, roof structure and interior framing are engineered to not burn.

To understand why that matters, consider this: traditional wood-frame homes ignite at around 600°F and create what fire scientists describe as a domino effect. Once one goes, the next follows. It's why the 2025 Palisades and Eaton fires moved the way they did, consuming entire blocks in hours. Concrete panel construction doesn't propagate fire that way. The material simply doesn't behave like wood.

A non-combustible home in a fire zone represents a measurably different risk category than a wood-frame home on the same street. That difference shows up in premiums and in whether you can get coverage at all.

The concrete panel building systems we use also exceed California's Net-Zero Energy Mandate, integrating PV solar, advanced HVAC filtration and thermal energy storage. A home built with this technology isn't just more insurable. It's built for the next 50 years of California climate reality.

What Are the Real Fire-Resistant Construction Options for LA Rebuilds — and What Do They Cost?

This is the question we hear most often, and it deserves a direct answer. There isn't one right system. There's a spectrum of options, with real differences in cost, fire performance, insurability, and how the home looks and feels when it's done.

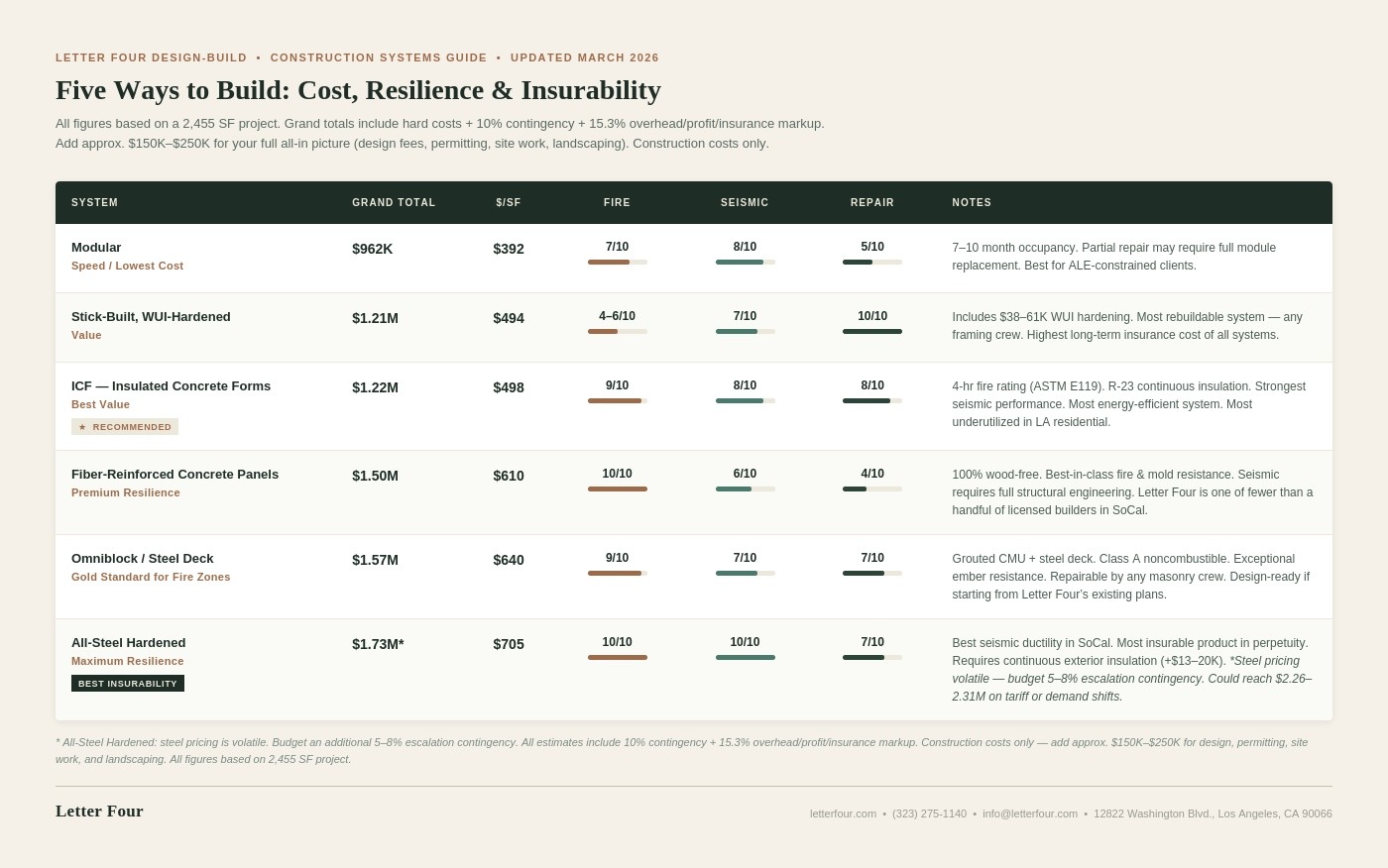

All figures below are based on a 2,455 SF project and include hard costs plus a 10% contingency cushion. Add approximately $150,000–$250,000 for your full all-in picture (site work, design fees, permitting, landscaping, etc.).

Here is what each system means in plain terms:

Modular: Speed and lowest entry cost

For homeowners constrained by additional living expense (ALE) timelines, modular construction's 7–10 month occupancy window is its single biggest advantage. The structural steel chassis provides solid fire and seismic performance. The trade-off: partial repair often requires replacing an entire module, which affects long-term repairability. Best suited to clients who need to get back into a home quickly.

Stick-Built, WUI-Hardened: Most familiar, highest long-term insurance cost

Wood-frame construction hardened to California's wildland-urban interface (WUI) requirements meets current code minimums with Class A roofing, enclosed eaves, tempered glass, and fire-resistant siding. The $38–61K WUI package is already built into this estimate. It's the most rebuildable system — any framing crew can work on it — but it carries the highest projected long-term insurance cost of all six systems. Meeting the baseline isn't the same as improving your risk profile.

ICF (Insulated Concrete Forms): Best value for resilience

ICF is the most underutilized system in LA residential construction, and the one we recommend most often to clients who want meaningful fire and seismic protection without moving to the top of the cost range. The four-hour ASTM E119 fire rating, R-23 continuous insulation, and reinforced concrete shear walls on all four sides give you exceptional performance at a price point just above stick-built. It's also the most energy-efficient system we build — a real advantage under California's net-zero energy mandate.

Fiber-Reinforced Concrete Panels: Premium fire resistance, fully wood-free

This system eliminates wood from the structural equation entirely: concrete panel walls, steel-bar joist roof systems, and commercial-grade metal interior framing. It achieves the highest fire resistance rating of any residential system and offers outstanding mold resistance — relevant given the water and smoke damage many fire survivors dealt with. Seismic performance requires full structural engineering, and the proprietary panel system has a lower repairability score than masonry-based alternatives. Letter Four holds a technology license for this system and is one of fewer than a handful of licensed builders in SoCal.

Omniblock: The gold standard for fire zones

Grouted CMU block construction paired with a steel deck roof is Class A noncombustible and has proven seismic performance. It's repairable by any masonry crew, which matters if you're thinking 20–30 years out. Letter Four has existing design plans ready for this system, which can reduce design time for eligible lots. A strong choice for clients who want proven, non-proprietary materials with excellent long-term repairability.

All-Steel & Fire Hardened: Maximum resilience, permanently insurable

Full structural steel construction provides the best seismic ductility in Southern California — yielding rather than brittle shear failure — and best-in-class fire performance. Insurers view this as the most favorable risk profile of any residential system, and it is designed to remain fully insurable in perpetuity. It requires continuous exterior insulation (an additional $13–20K) and offers the least architectural flexibility of the six systems, but for clients whose primary goal is long-term protection and insurability, nothing else comes close. Note: steel pricing is volatile — budget an additional 5–8% escalation contingency.

Where you land on this spectrum depends on your lot, your budget, your timeline, your insurance situation, and what home means to you. Some clients want to rebuild as faithfully as possible to what they lost. Some want to start fresh. Most want something in between: the warmth and character of the home they loved, built with materials that protect them going forward.

There is no single right answer, but there is a set of questions you need to be asking before you finalize your plans. The time to ask them is now, not after permits are pulled.

Why Does the Design-Build Model Matter More in a Fire Rebuild?

Rebuilding after the fires here in Los Angeles is not like a standard remodel. The regulatory environment is more complex. The insurance coordination is more demanding and the emotional stakes are higher. The decisions compound faster. What you choose in the design phase shapes what's possible in permitting, which shapes what gets built, which shapes what you can insure.

That's why the integrated design-build model we practice at Letter Four is particularly well-suited to fire rebuilds in the LA area. When architecture, interior design and construction management are handled by a single team under one roof, the friction that typically derails projects disappears.

Letter Four was co-founded by Lauren Adams, a licensed architect, and Jeremy Baker, a licensed general contractor. The firm holds architecture license #C30146 and contractor license #B1028949 in California. We've been doing design-build work in Los Angeles for over 15 years, and we came into the fire rebuild space because we saw what was happening to our neighbors and knew we had something real to offer.

We integrate advanced non-combustible structural systems, including fiber-reinforced concrete panel construction, during the design phase, building fire-resilient homes that are also architecturally distinctive and deeply personal. The goal isn't a bunker. The goal is a home that feels like yours, built to last.

We also help clients navigate the insurance and permitting landscape. We've worked through LA County's One-Stop Permit Centers, understand the updated WUI code requirements, and can help document your construction choices in ways that support your insurance conversations.

If you're ready to start that conversation, we're here. Book a free consultation with our team. We'll tell you what we know, and what your real path forward looks like.

Frequently Asked Questions

What does the State Farm rate hike mean for homeowners rebuilding after the LA wildfires? The March 2026 settlement allows State Farm to keep a 17% average rate increase for California homeowners. For those in high-risk fire zones like Malibu, Pacific Palisades and Altadena, some local increases exceed that average significantly. One Malibu homeowner's premium reportedly more than doubled in a single year. The deal pauses mass non-renewals through 2026, which provides some short-term stability, but it doesn't resolve ongoing claims disputes or reduce premiums. The bigger implication for rebuilders is this: insurers are pricing risk based on fire exposure, and that calculation isn't going to reverse. How you build your replacement home will have a direct bearing on what insurance looks like going forward.

Can building a fire-resistant home in Los Angeles lower my insurance premium? It can, and more importantly, it can affect whether you're insurable at all in the long term. Insurers don't just look at your zip code. They increasingly evaluate construction type, materials and fire-resistance ratings. Homes built with non-combustible materials, like the fiber-reinforced concrete panel systems we use, present a meaningfully different risk profile than wood-frame construction in the same fire zone. That distinction can translate into lower premiums, broader coverage options and better renewability. We recommend discussing your construction plans with your insurance broker before finalizing your rebuild design, so the decisions you make now work in your favor.

What is non-combustible home construction and is it right for a wildfire rebuild? Non-combustible construction uses materials that don't ignite or sustain fire, primarily concrete, steel and fiber-composite systems, in place of traditional wood framing. At Letter Four, we offer this technology for LA wildfire rebuilds using fiber-reinforced concrete panel walls, steel-bar joist roof systems and commercial-grade metal interior framing, eliminating the wood that makes conventional homes so vulnerable to fire spread. These homes don't just resist fire better. They don't contribute to the neighborhood-level domino effect that makes California wildfires so destructive. Whether this is right for your rebuild depends on your site, budget and goals, which is exactly the kind of conversation we have with clients in our initial consultation.

How long does it take to get a permit to rebuild after the LA wildfires? As of early 2026, LA County's fire-zone permitting is averaging roughly 100 days, significantly faster than the 8 to 24 months typical for comparable projects outside designated fire areas. That's genuinely good news. The One-Stop Rebuild Centers for Palisades and Altadena have streamlined the process considerably. That said, the timeline still depends on the completeness of your application, compliance with updated WUI fire codes, site-specific requirements and the volume of applications ahead of yours. Working with an experienced design-build team that understands the permitting process and can submit clean, code-compliant drawings the first time is the most reliable way to avoid delays.

What is the difference between a design-build firm and hiring an architect and contractor separately for a fire rebuild? When you hire separately, you're managing the relationship between your architect and contractor yourself. You bear the cost of any miscommunication, scope gaps or design-to-construction translation errors. In a fire rebuild, where decisions compound quickly and the margin for error is low, that friction is expensive. A design-build firm like Letter Four integrates architecture, interior design and construction under one team. That means the people designing your home are in direct communication with the people building it, from day one. Pricing is more transparent, timelines are more predictable, and you have one point of contact for the entire project rather than two or more professionals pointing at each other when something goes wrong.

Is it worth rebuilding in a California wildfire zone, or should I sell? This is one of the most personal decisions a homeowner can face, and we won't pretend there's a universal right answer. What we can tell you is that the calculus is shifting. At least 600 property owners in LA fire zones have already chosen to sell rather than rebuild, largely because of insurance uncertainty and construction costs. For those who want to come back, fire-resistant construction is changing what's possible: better insurability, stronger resale value and homes designed to withstand the fire conditions that have already proven they can reach these neighborhoods. If you're trying to decide, a no-pressure consultation with our team is a reasonable first step.

Sources: Los Angeles Times / Tribune Content Agency (March 7, 2026); Insurance Journal (March 9, 2026); The Daily Economy (February 2026); Milken Institute (January 2026); McKinsey & Company (January 2026); Pro Builder Magazine; Governor of California (July 2025).

.svg)

.png)